The workflow, screen by screen

Trevor quoted a real Saint Petersburg property live, from address to bound-ready policy, in a couple of minutes. Faces and meeting chrome cropped out; these are the shared screens only.

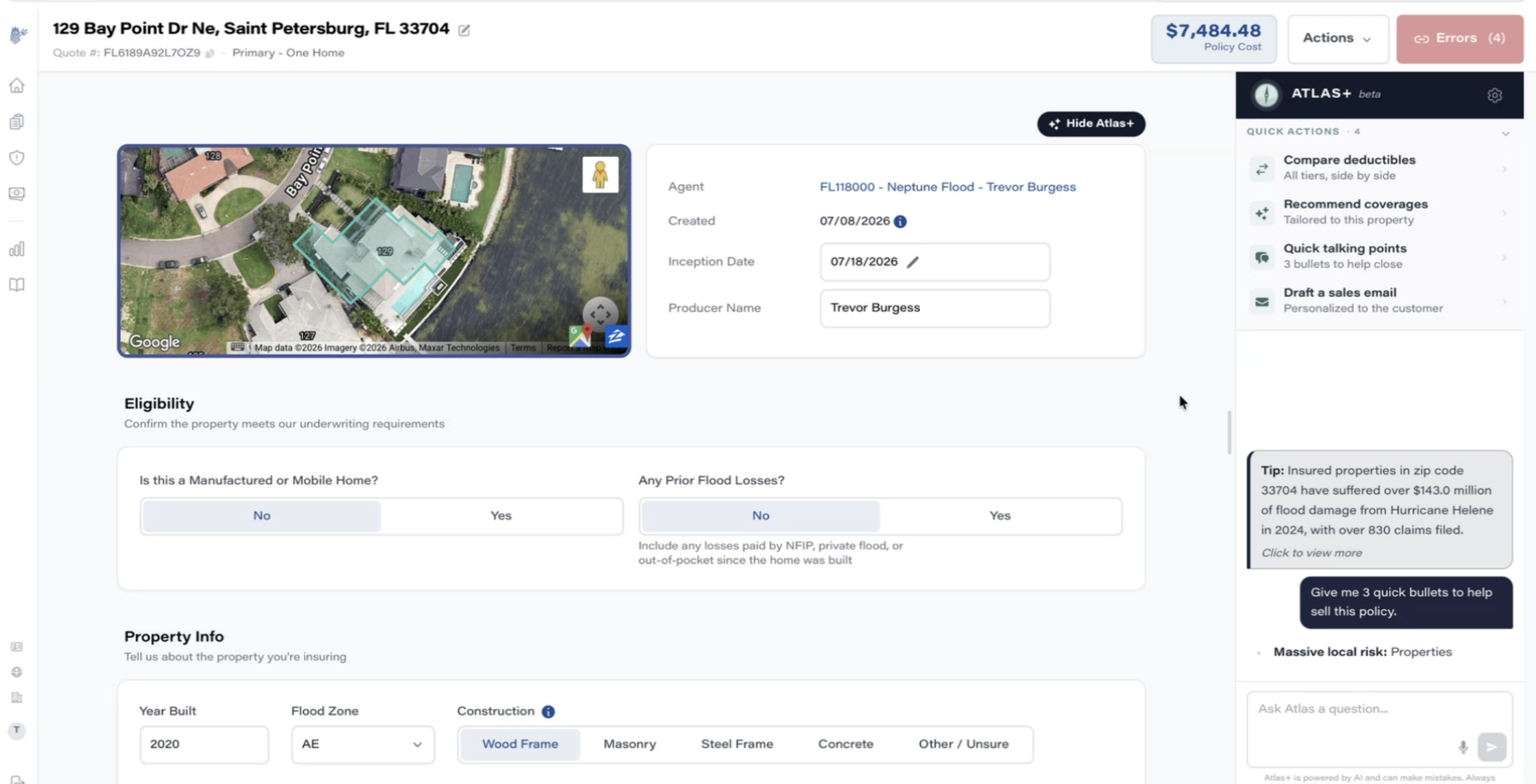

Address, aerial map with the parcel outlined, agent attribution, and the live policy cost pinned to the header. Note the error model: instead of blocking, a red Errors (4) counter sits where Bind will eventually be. Atlas+ (their AI copilot) opens with proactive local context: properties in zip 33704 took $143M in flood damage from Hurricane Helene, 830+ claims.

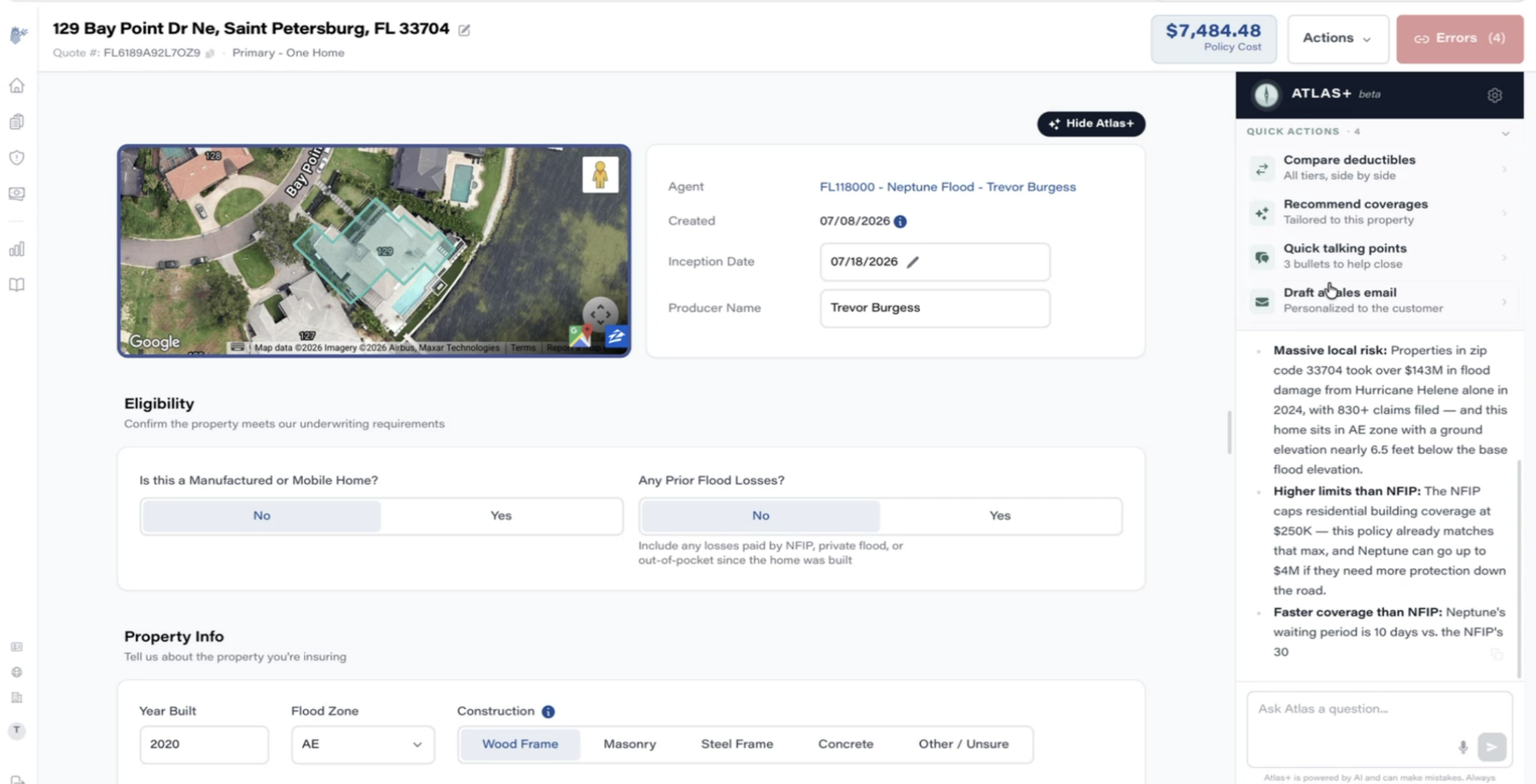

"Give me 3 quick bullets to help sell this policy" → massive local risk, higher limits than NFIP ($250k cap vs Neptune's $4M), 10-day vs 30-day waiting period. Trevor's framing: this "helps the agent feel smart talking about flood" and drives close rates. Quick actions include compare deductibles, recommend coverages, and draft a personalized sales email.

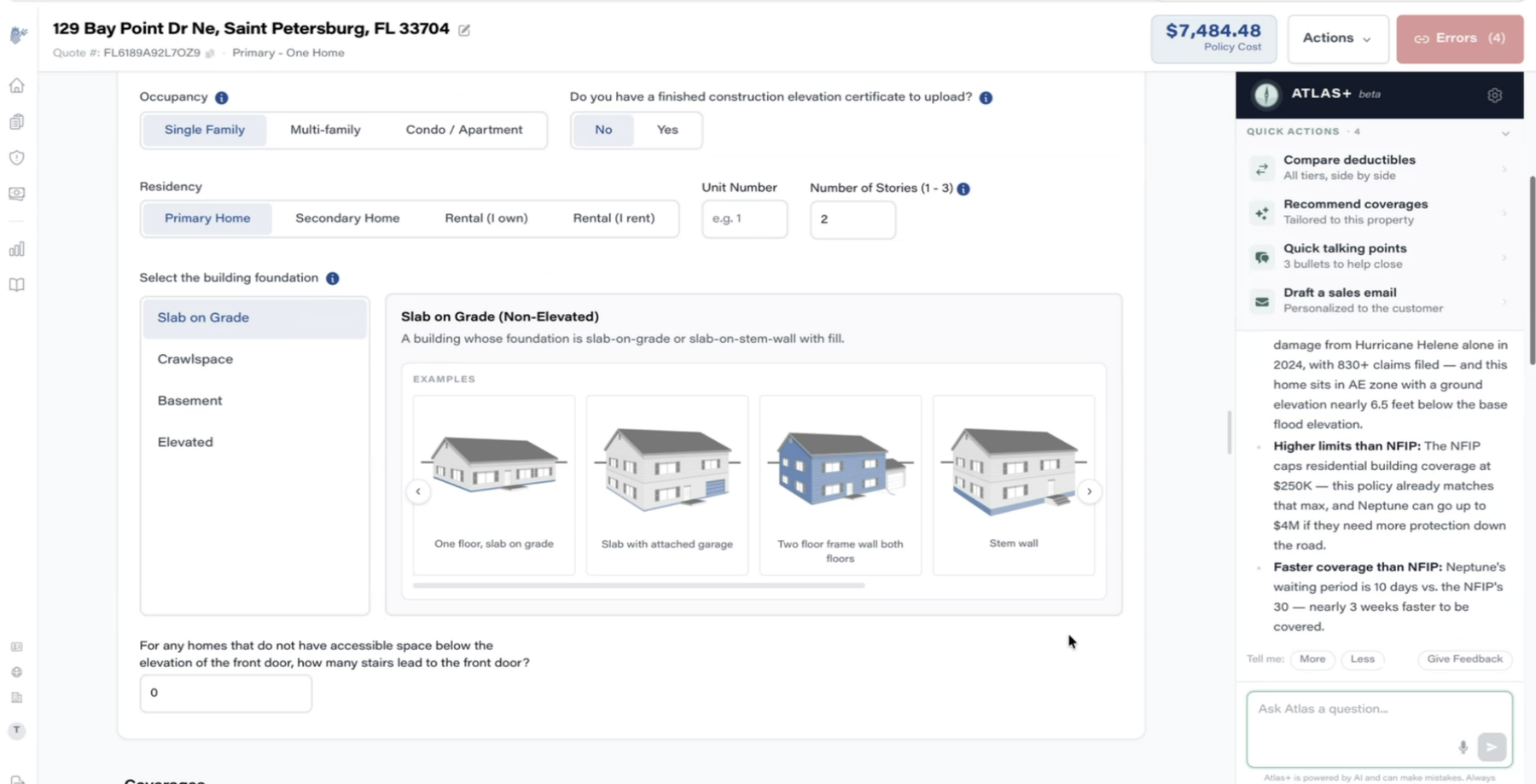

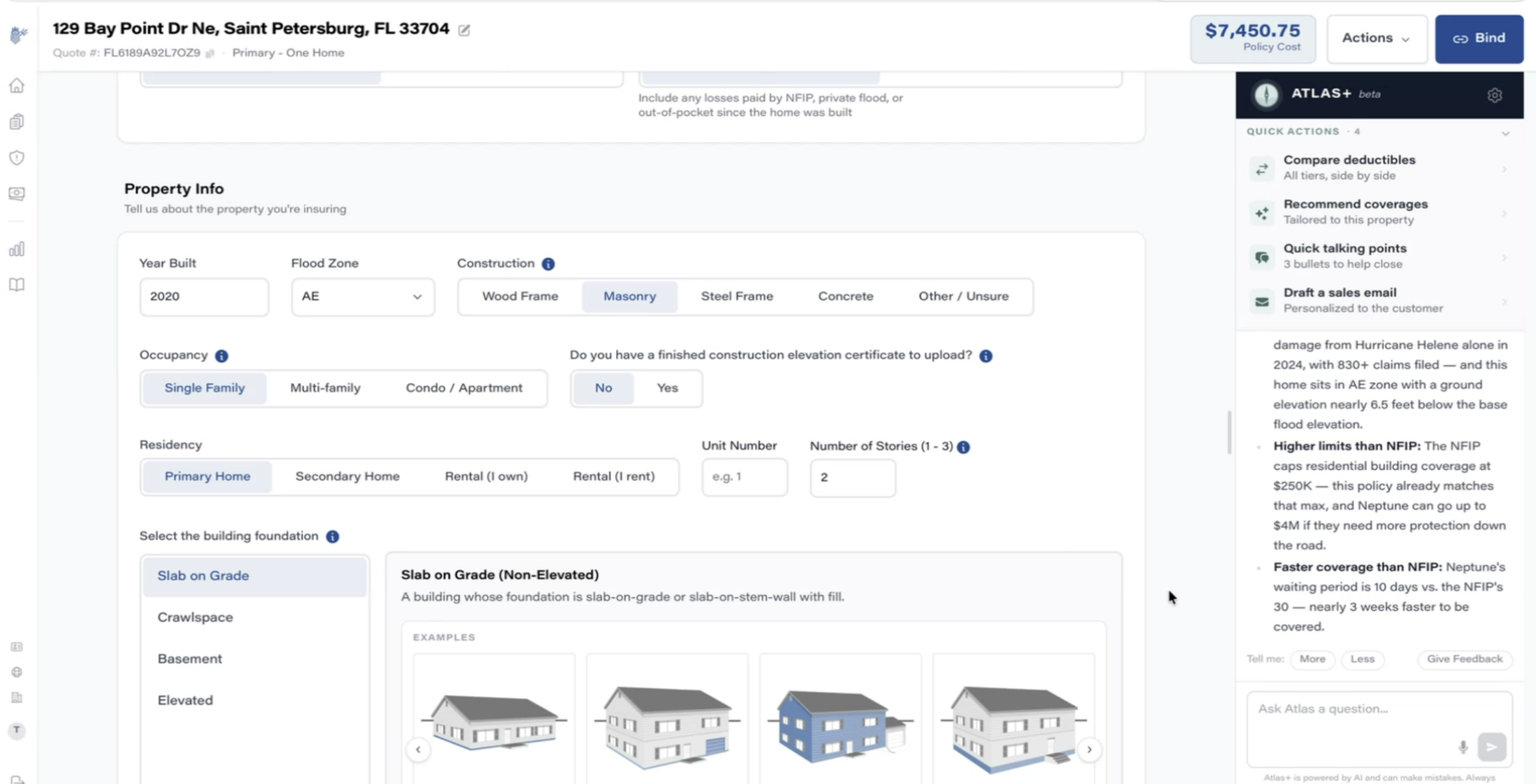

The foundation question — where customers usually stumble — is answered with an illustrated picker (slab, crawlspace, basement, elevated, each with example drawings). Everything defaults sensibly; the agent only refines.

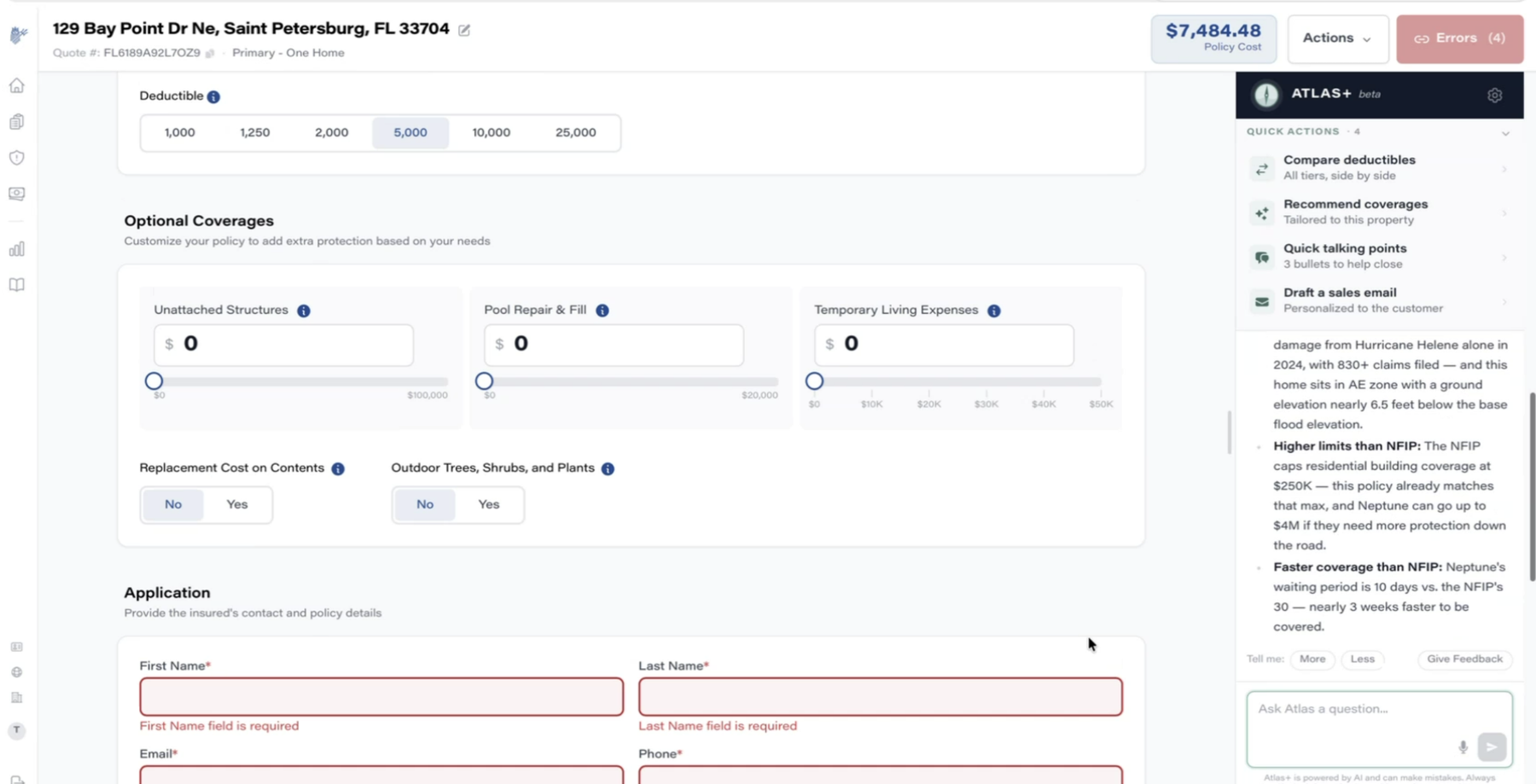

Required fields show inline errors, and the header counter ticks down as they're resolved — Errors (4) → (2) → Bind. The quote and price exist the whole time; completeness only gates the final action, not the exploration.

Switching construction Wood Frame → Masonry updates the header price in place ($7,484 → $7,451). No "recalculate" button, no page reload — the Google Flights lever model we keep referencing.

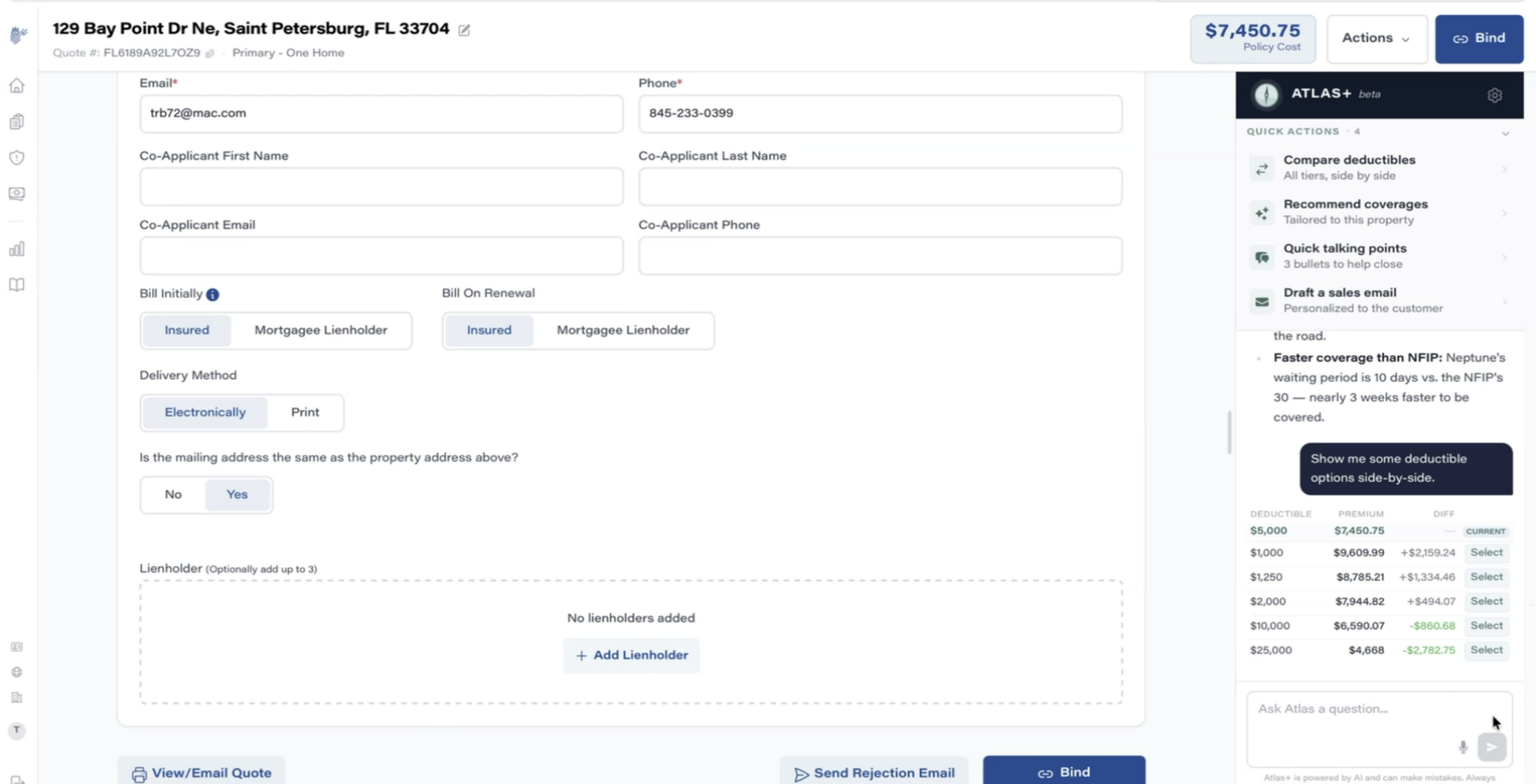

"Show me some deductible options side-by-side" → a compact table of every tier with premium and delta ($1k = +$2,159 … $25k = −$2,783), each with a one-click Select. This is the most common live-call negotiation (customer asks "what if the deductible were higher?"), served in seconds.

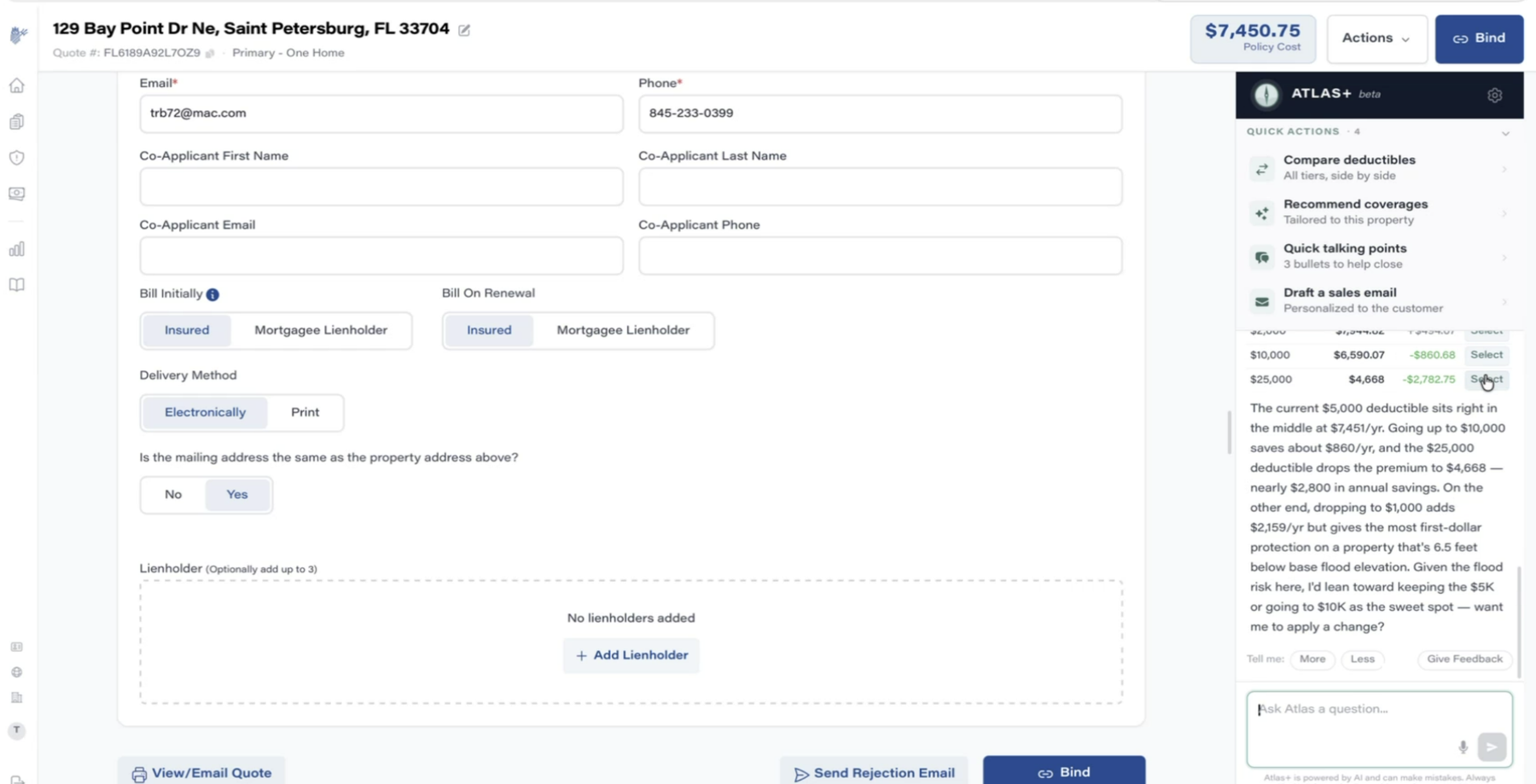

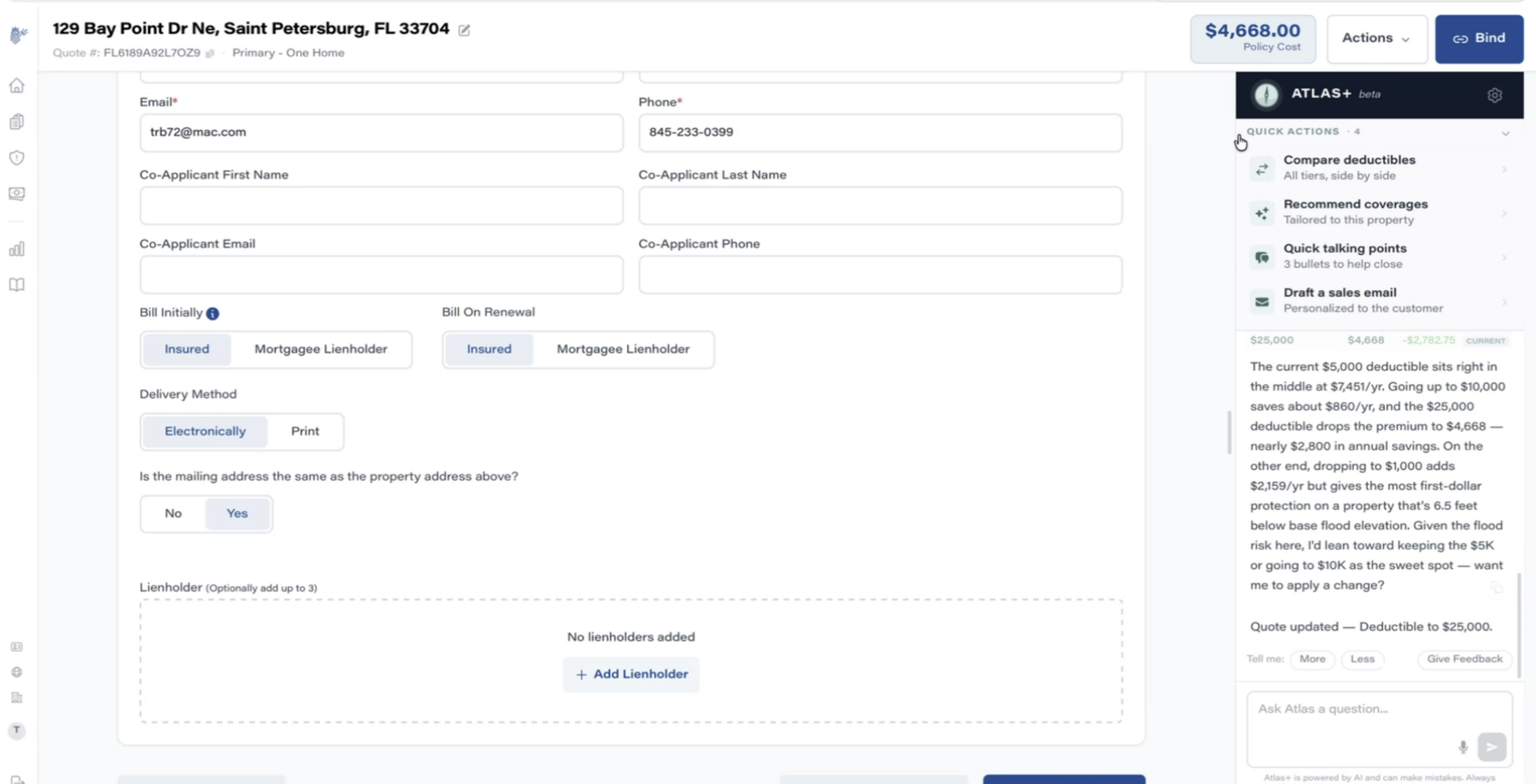

Atlas doesn't stop at the table — it narrates the trade-off (the property sits 6.5 ft below base flood elevation, so first-dollar protection matters) and lands on a stance: keep $5k or go $10k. Then: "want me to apply a change?"

The agent says yes, and Atlas edits the quote itself — "Quote updated — Deductible to $25,000", header reprices to $4,668. This is the agentic step beyond our current Ray patterns: conversational panel + the ability to safely mutate the working quote.

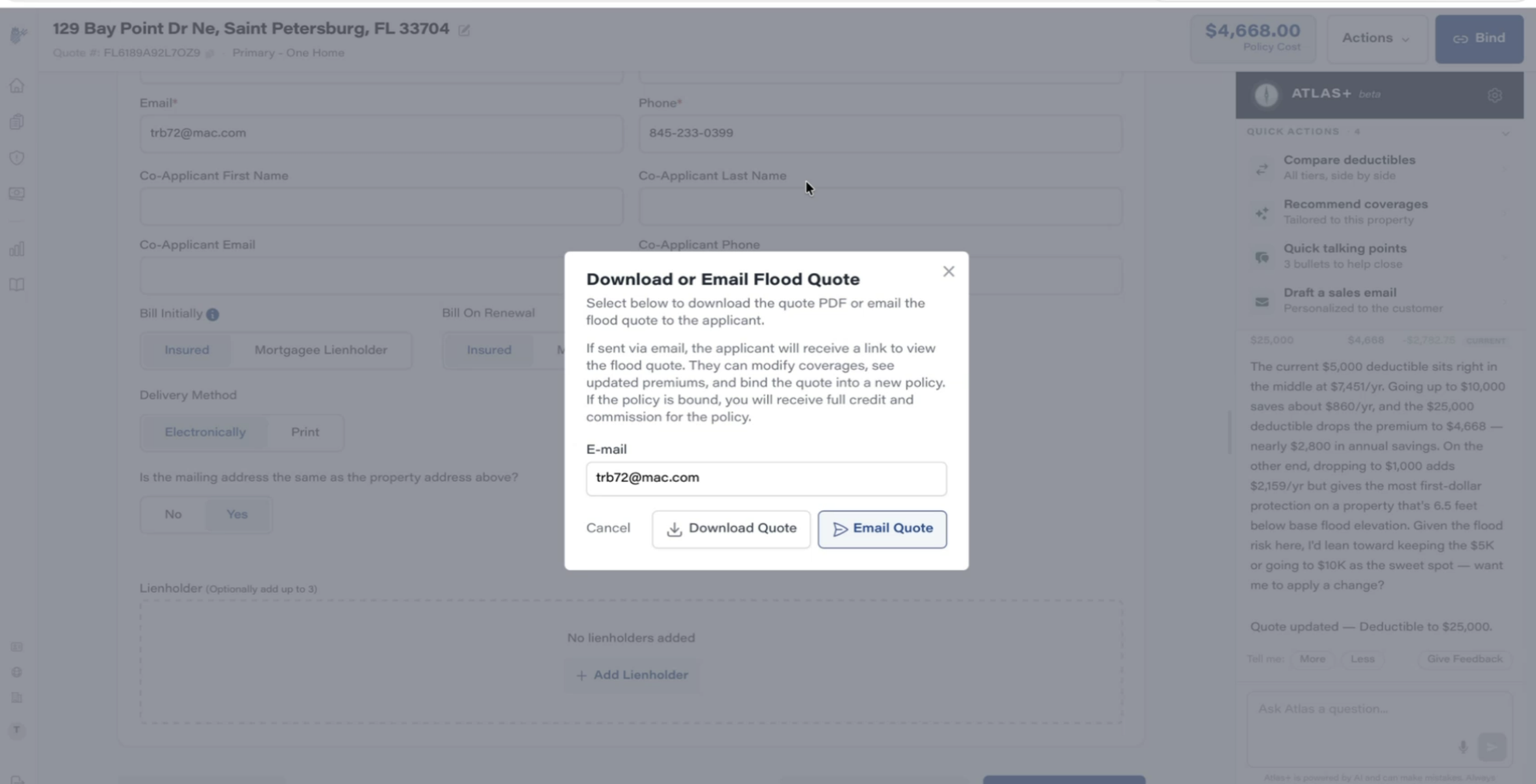

Email the quote and the customer gets a link where they can adjust coverages, watch the premium update, and bind on their own — with the originating agent keeping full credit and commission. Self-service that doesn't disintermediate the agent.

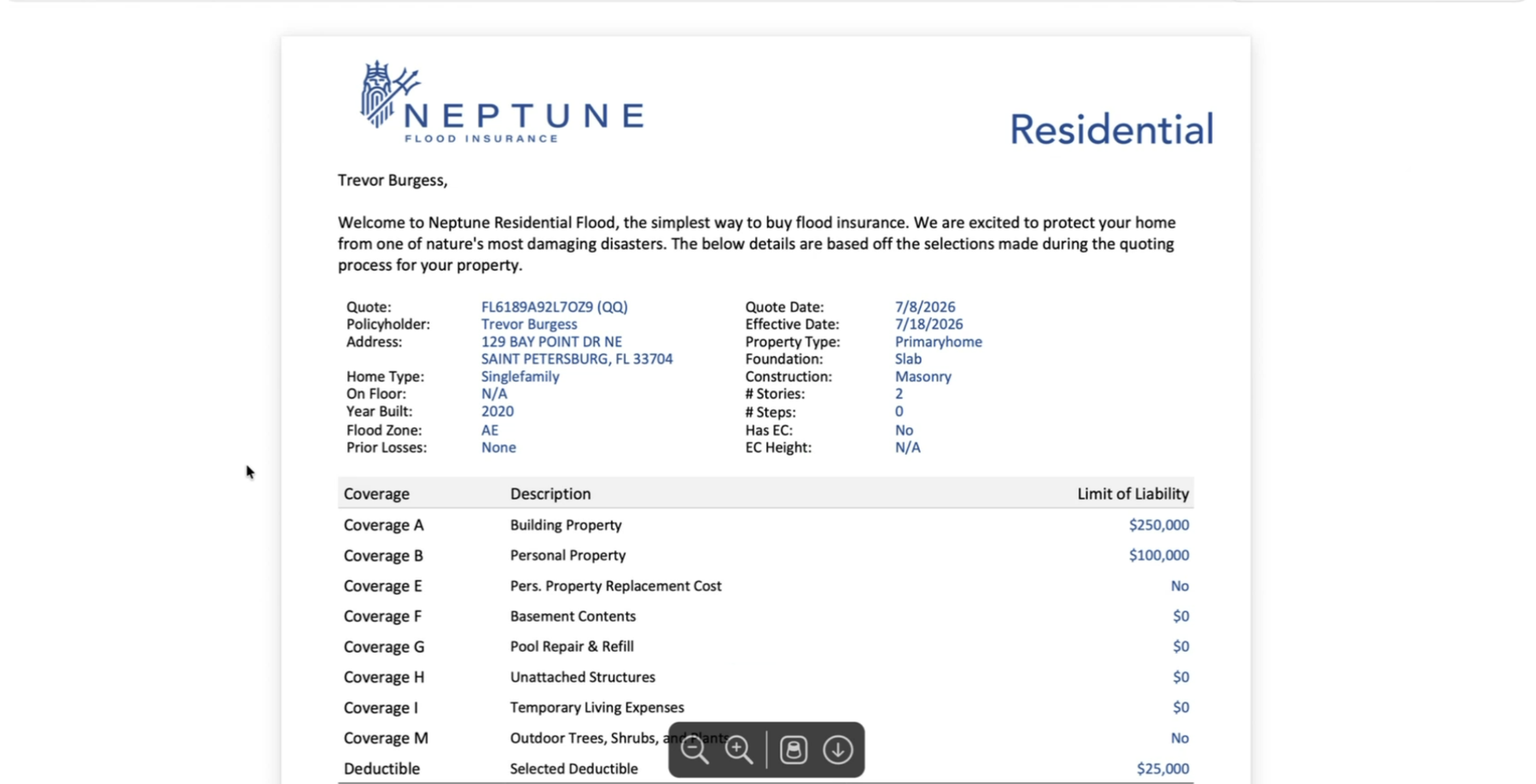

Clean one-pager: property characteristics, coverage schedule A–M, selected deductible, and total annual cost. Familiar shape for anyone who's read a dec page — easy for advisors to walk a customer through.

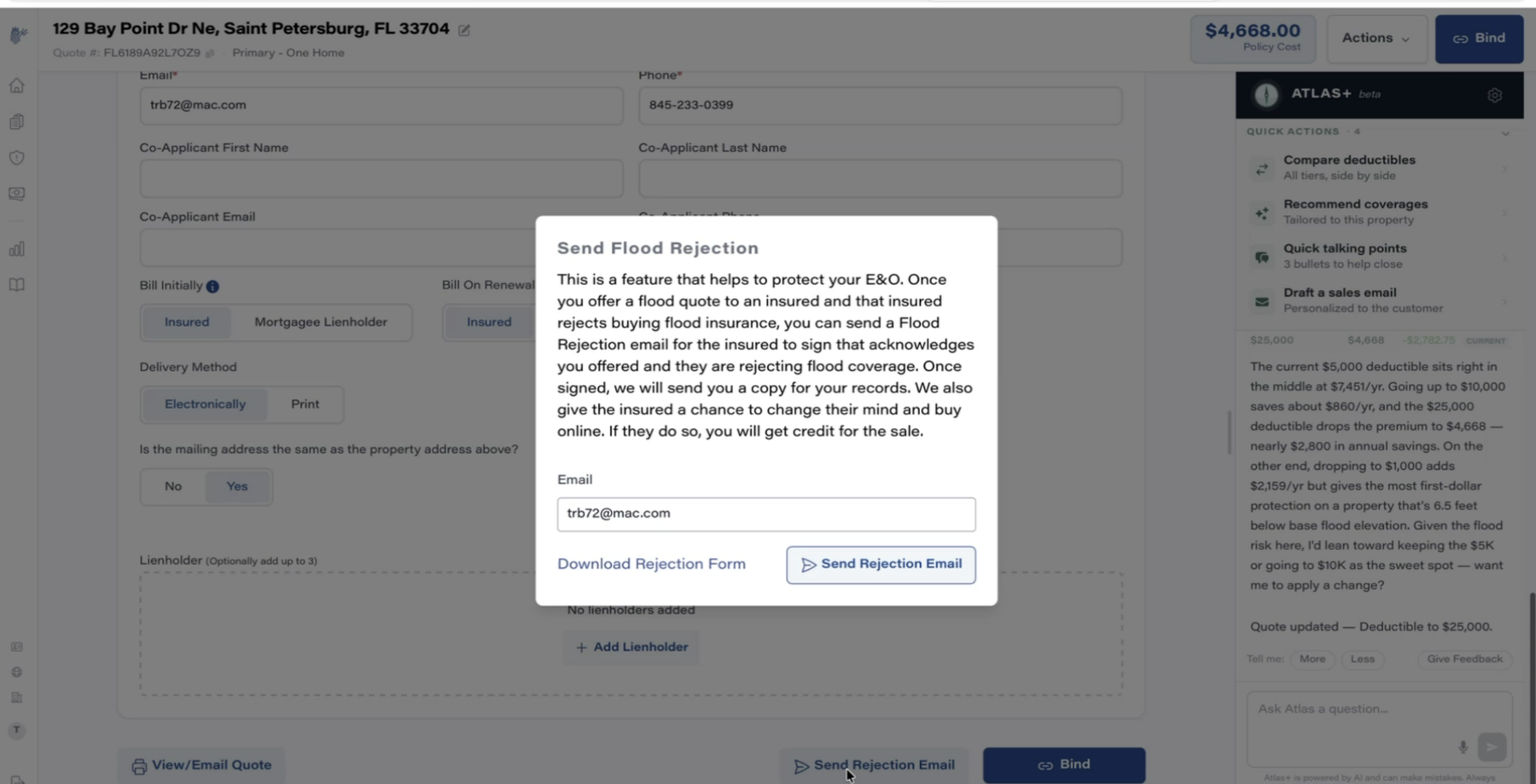

If the customer declines flood, the agent sends a Flood Rejection email: the insured signs an acknowledgment that coverage was offered and refused — E&O protection with an automatic audit trail. And the email gives them one more chance to change their mind and buy online (~20% do). Also available as a raw form via API if we'd rather run it through our own comms.

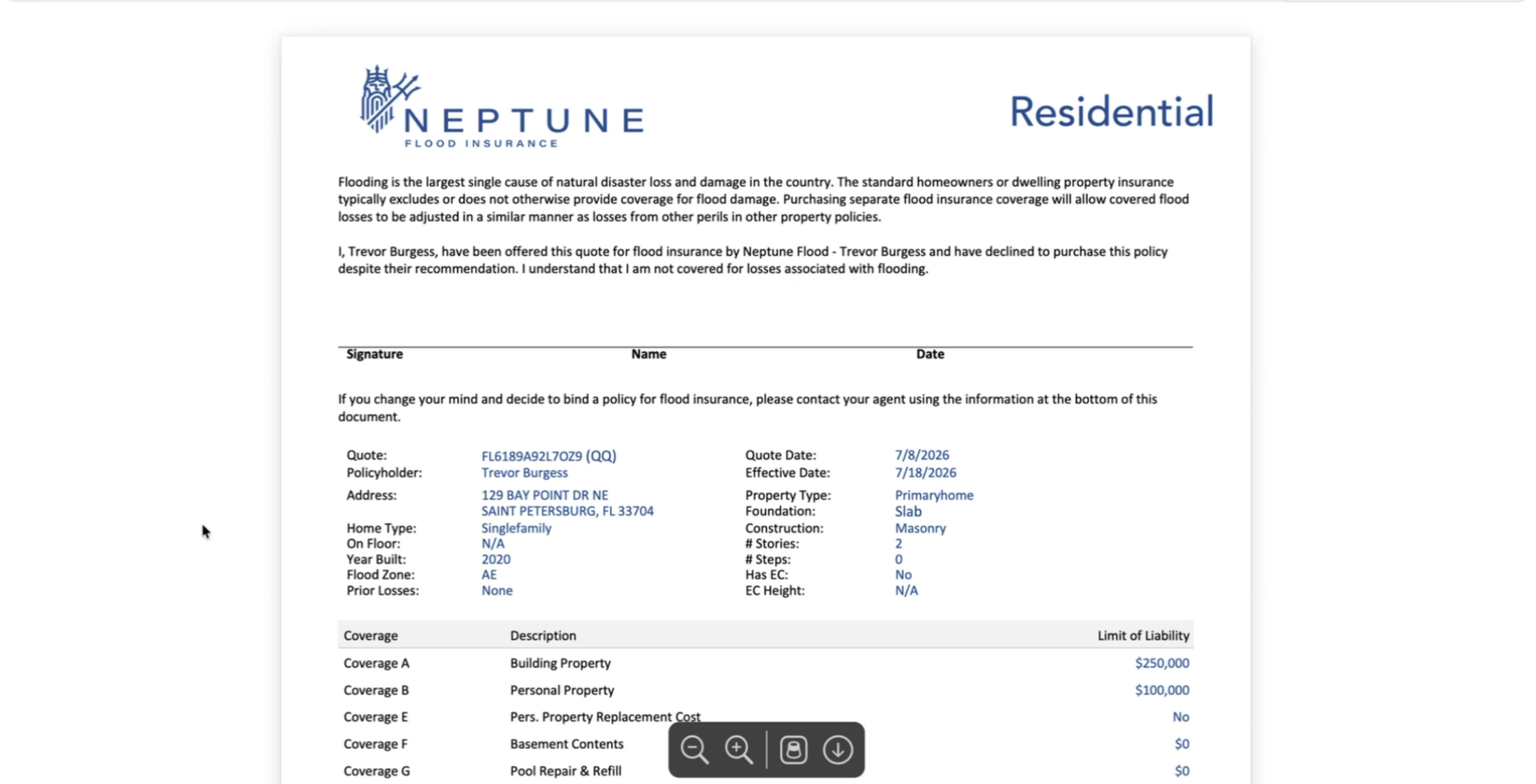

"I have been offered this quote … and have declined to purchase this policy. I understand I am not covered for losses associated with flooding." Signature, name, date — plus the full quote details below so the declined offer is unambiguous and recoverable.